Tokens Offered Under the ICO and Estonian Regulations Applicable to Them

This article contains the information that can be very useful for entities engaging with virtual currencies and ICOs.

Mining Cryptocurrencies

What regulations apply to this activity?

Mining cryptocurrencies as a field of activity does not fall under the supervision of Estonian Financial Supervision Authority (EFSA). However, we recommend paying attention to the tax aspects. We refer to the publication of Estonian Tax and Customs Board on the taxation of income from cryptocurrencies. If you have any questions, please contact Estonian Tax and Customs Board directly.

Virtual Currency Exchange Service or Wallet Service

I want to offer a virtual currency exchange service or wallet service. What permits do I need to apply for?

The purchase and sale of virtual currencies may be subject to anti-money laundering regulations. Therefore, it is necessary to take into account Section 70 (1) 4), 5) and Section 71 of the Prevention of Money Laundering and Terrorist Financing Act (Money Laundering), according to which, in order to offer the service of exchanging virtual currency into fiat currency and the service of a virtual wallet, a relevant permit must be issued by Financial Intelligence Unit. The government fee payable for the application is €3300. In accordance with Section 71 of the Money Laundering Act, the Financial Intelligence Unit shall consider the application for registration within 60 days from the date of submission of the application. By decision of the Financial Intelligence Unit, the period for issuing an activity permit may be extended up to 120 days. No services may be offered prior to the issuance of the permit.

According to the MLTFPA, the authorisation requirement does not apply to:

- a person who holds an authorisation from EFSA;

- a person who is required by another law to apply to EFSA for an authorisation;

- a person who holds an authorisation from a financial supervisory authority of a country of the European Economic Area allowing to operate through a branch in Estonia or cross-border and EFSA has been notified of such activity;

- a person who offers the services referred to in section 70 (1) of the MLTFPA.

Token (Public) Offering (ICO)

I would like to organize a token (public) offering (ICO). What rules apply to this activity?

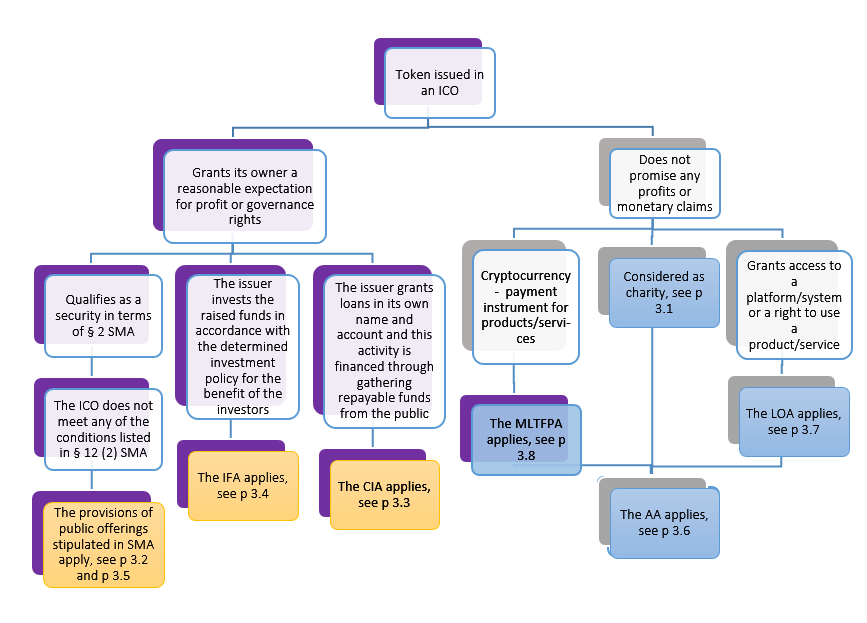

The first step is to analyze the rights granted by the tokens to determine whether or not they are securities within the meaning of Section 2 of the Securities Market Act. Depending on the outcome of the analysis, the offering of tokens may or may not need to be registered with the EFSA.

Tokens are classified as securities if, for example, they can be transferred (as a property right, obligation or contract) on the basis of at least a unilateral expression of will, or if they grant voting or decision-making rights in the issuer or give the investor a certain expectation of return in relation to his investment (e.g. a right to share of the issuer's profits, regular cash flows, or some other promise of future profit), regardless of whether the funds raised are repayable by a maturity date or there is no maturity date (e.g. a perpetual bond).

Donations

A fundraising for the development of a business project is considered a donation only on the condition that it does not result in (i) an interest in the issuer or (ii) an obligation to repay the funds, interest, dividends or other repayments or cash flows. In addition, no right to use a service or product must arise in connection with the donation.

Donation description materials must clearly state that the donation is a gift and that donors are acting in good faith and knowingly giving up their contribution. For more information on the taxation of donations, please visit Estonian Tax and Customs Board.

The Securities Market Act (SMA) and the Obligation to Prepare a Prospectus

To the extent that tokens offered in an ICO qualify as securities, the provisions of SMA on the offer of securities and the provision of investment services apply. It is necessary to consider whether the offer itself is an offer of securities to the public within the meaning of Section 12(2) of SMA.

An offer of securities shall not be deemed to be public if:

- the offer of securities is directed exclusively to qualified investors, or

- an offer of securities is made to fewer than 150 persons per Contracting State who are not qualified investors, or

- an offer of securities is addressed to investors acquiring securities for a total amount of at least €100,000 per investor for each individual offer, or

- an offering of securities with a par value or book value of at least €100,000 per security is made, or

- an offering of securities with an aggregate consideration of less than €2,500,000 for all Contracting States in the aggregate, calculated over a period of one year following the offering of the securities.

If none of the above conditions exist, the offer is deemed to be a public offer, in which case a prospectus for the offer must be prepared and registered with the EFSA.

Pursuant to Section 17 (4) and (4) of SMA, in the case of an offer with a total consideration of less than €5,000,000, the prospectus must be drawn up in accordance with the Prospectus Regulation No. 809/2004/ EC of European Union (Prospectus Regulation) or a regulation issued by the competent minister.

In the case of public offerings with a total consideration of more than €5,000,000, the prospectus must be prepared in accordance with the aforementioned Prospectus Regulation.

All listing prospectuses must be prepared in accordance with the Prospectus Regulation. The level of detail of the prospectus depends on the qualification of the securities to be offered.

For example, the Prospectus Regulation provides for slightly different requirements for public offerings of securities and bonds. Estonian law does not currently provide for any exemptions (or other specific provisions regulating ICOs) from the existing Securities Ordinance.

However, the Prospectus Regulation grants some exemptions for start-up companies in preparing a prospectus. These are companies that have been in existence for less than three years. The adjustments to the minimum disclosures are set out in Article 23 of Prospectus Regulation. More detailed descriptions can be found in the document "ESMA Update of the CESR recommendations. The consistent implementation of Commission Regulation (EC) No. 809/2004 implementing Prospectus Directive" (20 March 2013) and "ESMA Q&A Prospectuses" (October 2017).

A decision on the registration of a prospectus of an issuer whose securities are not yet admitted to trading on a regulated market or which has not yet offered securities to the public shall be taken at the latest within 20 (twenty) working days of the submission of the legally compliant prospectus. The overall duration of the procedure for registering a prospectus depends on various factors. In practice, the procedure can take around 36 months, depending on the original quality of the prospectus, whether it needs to be amended and the speed with which the necessary amendments are made.

Please also refer to Section 4.3.3 Credit Institutions Act (CIA). A company offering tokens may also be subject to CIA and the licensing requirement for credit institutions under the Act. This applies if the company makes loans on an ongoing basis in its own name and for its own account and the financing of this activity from ICOs is made by raising repayable funds from the public. Such activity may qualify as that of a credit institution or bank for which authorisation must be sought from EFSA.

EFSA has previously published in its memorandum "The Field of Activity of Credit Institutions" that the solicitation of repayable funds from the public may qualify as an offer of securities under certain conditions.

Investment Funds Act (IFA)

Depending on the specific design and objective of an ICO, the Investment Funds Act (IFA) may be applicable - for example, where investors' capital is raised in an ICO with the aim of investing it further for the benefit of investors and in their collective interest in accordance with the established investment policy. Section 2 (3) of the IFA requires such fund to have a fund manager.

Section 3 (1) of the IFA states that a fund manager is a company whose principal and continuing activity is the management of one or more funds.

A management company may manage a fund or funds incorporated or established under the IFA, including a fund incorporated or established under the laws of a foreign country.

Section 3(2) of the IFA requires a person to apply for a license to act as a fund manager or to register its activities with the EFSA in accordance with the provisions of Part 5 of the IFA. This is required regardless of the platform through which the funds are raised.

The IFA sets out different types of fund managers and distinctions depending on whether the units of the investment fund are offered to the public or not. A useful material for the qualification of an investment fund is the ESMA Guidance "Guidance on the implementation and interpretation of the directive on alternative investment fund managers".

Securities Register Management Act (SRMA)

Pursuant to Section 2 (1) of the SRMA, the following securities must be entered in the register:

- Debt securities issued by a legal entity under private law registered in Estonia, the prospectus of which must be registered with the EFSA for a public offering in accordance with the Securities Market Act;

- Units and shares of investment funds registered in Estonia and admitted to trading on a regulated securities market or in a multilateral trading facility;

- Subscription rights for shares and for securities subject to registration, issued or offered to the public.

Advertising Act (AA)

When advertising an ICO, it is important to pay careful attention to the use of terms in advertising and the general advertising requirements set out in Chapter 2 of AA.

The advertisement must provide a clear and truthful representation of the product or service to the target audience. In particular, the advertisement must not be misleading as to the characteristics of the product or service offered. For example, advertising an investment service without the necessary authorization could be unlawful (as in the provisions § 3 (4) 11) and 16); § 4 (1) and § 29 (1) and (3) of AA).

A Utility Token may not be advertised as an investment or investment property.3.7 Law of Obligations (LOA). An ICO, where the tokens offered to give their purchasers access to a product or service, is essentially an upfront payment for a product or service. Consequently, taking into account that the contracts concluded in the context of an ICO use means of communication (a computer network), such ICOs are subject to the provisions of LOA on distance contracts concluded through means of communication and computer networks.

According to Section 54 and 62 superscript 1 (2) and 62 superscript 2 (1) of the LOA, the person organising an ICO must inform investors about the main features of the subject matter of the contract, the total price of the subject matter of the contract, including taxes, the duration of the contract or the conditions of its termination and other rights and obligations arising from the contract and its technical stages. This information must be highlighted and clearly stated.

In the event of withdrawal from the contract, Section 56 superscript 1 (1) of the LOA obliges the token issuer to return to the consumer (investor) everything received under the contract.

Money Laundering and the Law on the Prevention of the Financing of Terrorism (MLTFPA)

If the tokens are to be used solely as a means of payment for the purchase of goods or services or as a means of transferring money or value, they shall be considered payment tokens. Such tokens do not give rise to any claims against their issuer.

The definition of payment tokens corresponds to that of a virtual currency in the provision of Article 3(9) of MiFID, being a value represented in digital form which is digitally transferable, storable or tradable and which natural or legal persons accept as a means of payment, but which is not a legal tender of a country or fund within the meaning of Article 4(25) of Directive (EU) 2015/2366 of the European Parliament and of the Council on payment services in the internal market amending Directives 2002/65/ EC, 2009/110/ EC and 2013/36/EU and Regulation (EU) No. 1093/2010 and repealing Directive 2007/64/ EC (OJ L 337, 23.12.2015, p. 35-127) or a payment transaction within the meaning of Article 3 (k) and (l) of that Directive.

Issuers of payment tokens where payments are also accepted in fiat money should, at a minimum, comply with the due diligence requirements provided for in the MLTFPA.

I Trade / Invest in Tokens. Do I Need a Permit for These Activities?

An activity permit for an investment firm is required if the tokens qualify as securities and the firm provides one or more of the following services as a continuous activity:

- Receiving and transmitting orders in relation to tokens;

- Executing the orders in relation to Tokens on behalf of or for the account of the client;

- Trading tokens for its own account;

- Managing a portfolio of securities (consisting of tokens);

- Providing investment advice in relation to Tokens;

- Guaranteeing tokens or guaranteeing the offer, issue or sale of tokens;

- Organising an offering or issuance of tokens (organising ICOs);

- Operating a multilateral trading facility that brings together the non-concurrent or concurrent interests of different persons for the acquisition and transfer of securities under non-discretionary terms that result in a contract;

- Operating an organised trading facility.

There is no licencing requirement for investment firms provided that the circumstances set out in section 47 of SMA are present. The operation of a multilateral trading facility or an organised trading facility should not be construed as a mere display of interest in the acquisition and transfer of tokens where the relevant website does not permit such transactions. However, if the person displaying the transactions is the other party to the transaction, Section 42 (1) 3) of SMA, i.e., this qualifies as trading in tokens for his own account.

It should also be noted that such firms must comply with the provisions of Part 3 of SMA in addition to having an appropriate licence.

I am Planning an ICO and Would Like to Contact EFSA in This Regard. What Preliminary Information Should I Provide and What Do I Need to Consider in My Analysis?

In order to receive feedback or discuss a specific ICO and the legislation applicable to it, it is important that EFSA has analysed at least the following information in advance:

- name of the project for which funds are to be raised;

- name and contact details of the project company/ ICO organiser;

- timeline of the project: fundraising schedule, project implementation milestones;

- description of the product/service developed/offered (main features);

- which investors is the ICO aimed at?

- will there be any restrictions for investors?

- what technological solutions will be used in the project/ICO?

- in what (virtual) currency and how is it possible to invest in the project?

- what is the volume of the ICO?

- how and where will the funds be allocated?

- will a new token be created as part of the ICO? How?

- when and how will the token be transferred to the investor?

- what are the features and functions of the token?

- what rights does the token grant to the investor?

- how will compliance with the MLTFPA be ensured in relation to the ICO?

- how and where is it possible to sell or buy the token later?

- can the token be used to purchase products/services or make payments to third parties?

- does the token issuer plan to buy back the tokens?

The Consequences of Non-Compliance With the Legal Framework

Failure to comply with the above legal framework or providing false information in an ICO can be classified as fraud. In particular, as investment fraud within the meaning of Section 211 of the Penal Code (PC) or as the exercise of an economic activity without a corresponding permit within the meaning of Section 372 of the PC. In addition, various administrative offences may apply in the financial sector.

Disclaimer

Please note, the above instruments are still evolving and their legal framework and interpretative practice (including the relevant legal framework at EU level) may change. Therefore, EFSA reserves the right to modify or amend the current interpretation.

Recommendations

As there are numerous circumstances to be considered when organising an ICO, we recommend consulting an appropriate legal expert.

Specialists from AlphaLAW will be happy to help you organising an ICO and obtaining a cryptocurrency license in Estonia. Our assistance includes the preparation of the list of required documents, help in developing company procedural rules, translation of documents into Estonian/English and support throughout the whole licensing process.

In case you have any questions or are interested in organising an ICO or obtaining an Estonian license to exchange cryptocurrencies and other virtual assets for a fiat currency (crypto license in Estonia), please contact us through the following communication channels.